Annual Financial To-Do List

Things you can do for your future as the year unfolds.

What financial, business, or life priorities do you need to address for the coming year? Now is an excellent time to think about the investing, saving, or budgeting methods you could employ toward specific objectives, from building your retirement fund to managing your taxes. You have plenty of choices. Here are a few ideas to consider:

Can you contribute more to your retirement plans this year? In 2022, the contribution limit for a Roth or traditional individual retirement account (IRA) is expected to remain at $6,000 ($7,000 for those making “catch-up” contributions). Your modified adjusted gross income (MAGI) may affect how much you can put into a Roth IRA. With a traditional IRA, you can contribute if you (or your spouse if filing jointly) have taxable compensation, but income limits are one factor in determining whether the contribution is tax-deductible.1

Keep in mind, this article is for informational purposes only and not a replacement for real-life advice. Also, tax rules are constantly changing, and there is no guarantee that the tax landscape will remain the same in years ahead.

Once you reach age 72, you must begin taking required minimum distributions from a traditional Individual Retirement Account in most circumstances. Withdrawals from Traditional IRAs are taxed as ordinary income and, if taken before age 59½, may be subject to a 10% federal income tax penalty.

To qualify for the tax-free and penalty-free withdrawal of earnings, Roth 401(k) distributions must meet a five-year holding requirement and occur after age 59½. Tax-free and penalty-free withdrawal can also be taken under certain other circumstances, such as the owner’s death. Employer match is pretax and not distributed tax-free during retirement.

Make a charitable gift. You can claim the deduction on your tax return, provided you follow the Internal Review Service guidelines and itemize your deductions with Schedule A. The paper trail can be important here. If you give cash, you should consider documenting it. Some contributions can be demonstrated by a bank record, payroll deduction record, credit card statement, or written communication from the charity with the date and amount. Incidentally, the IRS does not equate a pledge with a donation. If you pledge $2,000 to a charity this year but only end up gifting $500, you can only deduct $500.2

Make certain to consult your tax, legal, or accounting professional before modifying your record-keeping approach or your strategy for making charitable gifts.

See if you can take a home office deduction for your small business. If you are a small-business owner, you may want to investigate this. You may be able to write off expenses linked to the portion of your home used to conduct your business. Using your home office as a business expense involves a complex set of tax rules and regulations. Before moving forward, consider working with a professional who is familiar with the tax rules as they relate to home-based businesses.3

Open an HSA. A Health Savings Account (HSA) works a bit like your workplace retirement account. There are also some HSA rules and limitations to consider. You are limited to a $3,650 contribution for 2022 if you are single; $7,300 if you have a spouse or family. Those limits jump by a $1,000 “catch-up” limit for each person in the household over age 55.4

If you spend your HSA funds for non-medical expenses before age 65, you may be required to pay ordinary income tax as well as a 20% penalty. After age 65, you may be required to pay ordinary income taxes on HSA funds used for nonmedical expenses. HSA contributions are exempt from federal income tax; however, they are not exempt from state taxes in certain states.

Pay attention to asset location. Tax-efficient asset location is one factor that can be considered when creating an investment strategy.

Review your withholding status. Should it be adjusted due to any of the following factors?

- You tend to pay the federal or state government at the end of each year.

- You tend to get a federal tax refund each year.

- You recently married or divorced.

- You have a new job, and your earnings have been adjusted.

Consider consulting your tax, human resources, or accounting professional before modifying your withholding status.

Did you get married in 2021? If so, it may be an excellent time to review the beneficiaries of your retirement accounts and other assets. The same goes for your insurance coverage. If you are preparing to have a new last name in 2022, you may want to get a new Social Security card. Additionally, retirement accounts may need to be revised or adjusted?

Are you coming home from active duty? If so, go ahead and check on the status of your credit and any tax and legal proceedings that might have been preempted by your orders.

Consider the tax impact of any upcoming transactions. Are you preparing to sell any real estate this year? Are you starting a business? Might any commissions or bonuses come your way in 2022? Do you anticipate selling an investment that is held outside of a tax-deferred account?

If you are retired and in your seventies, remember your RMDs. In other words, Required Minimum Distributions (RMDs) from retirement accounts. In most circumstances, once you reach age 72, you must begin taking RMDs from most types of these accounts.5

Vow to focus on your overall health and practice sound financial habits in 2022. And don’t be afraid to ask for help from professionals who understand your individual situation.

Citations

1. thefinancebuff.com, August 11, 2021

2. irs.gov, January 22, 2021

3. nerdwallet.com, July 31, 2020

4. irs.gov, September 8, 2021

5. irs.gov, May 3, 2021

Market Update 9-23-2021

Video Transcript:

Good afternoon everyone. It is Friday, December 11.

Unfortunately, it looks like we’re heading for another shutdown here in Pennsylvania and many other places… some businesses such as restaurants, gyms, etc etc. We’ll see where this goes.

We see that the government is going to shut down tonight at 12am if they do not extend the budget through the last week of December. Hopefully that budget will get extended past today by the Senate. We certainly don’t need to add that to wrapping up what has been crazy 2020 with all that is going on with COVID and how that seems to be worsening here as we haven’t seen it yet in this country. Worse than it was when we had to break out initially in the March, April time period.

So, we will all see where that goes all we can do is control our health, our safety. So, we’ll see how that plays out. As far as the economy goes, we continue to see the markets have been pretty strong, as I had mentioned in my last video, I felt that maybe everything had been priced in for the election and it was going to be pretty smooth sailing and that’s pretty much how it played out. We didn’t have a lot of volatility. We haven’t had much volatility since the election. We know that is contested but hopefully by Monday that will all be resolved as the electoral college casts their votes for whoever their state had voted to be the next president. And that should go pretty much as planned. The Supreme Court ruled in July on the validity of the electoral process of electing the president. It was a unanimous vote by the Supreme Court. So, it’s going to happen and it should have us having a new president in office come January.

Also, we see that, globally speaking, the economy has its “haves” and “have nots” as we know… industries that are thriving: housing, autos, construction, technology… and then we have the “have nots”: restaurants, travel, hotels, and real estate are suffering as far as commercial real estate because of the high vacancies. We’ll see where that goes here in the next six months… if it actually helps get everybody back in running somewhat normal as I like to say because I don’t think we’ll get back to normal on some of these things… maybe never… things that fundamentally change the way we live and do things, but again, time will tell.

Charts around the globe are very strong indicating strength in the markets. We have a ton of new monetary policy being put into the mix this week. Japan added $700 billion in new stimulus to what was already 2,200 billion in stimulus that they’ve already injected into the system. We see that the European Central Bank said they expanded their emergency repurchase program by another $500 billion this week. So, when we add it all up, there’s been about $12 trillion injected into the global economies to keep the flow of money going the velocity of money, as it is called moving so that we don’t have major collapses to add to the issues that we have from the pandemic. Those commitments look like they’re set in place at least until 2022. And as I’ve been mentioning in many videos, I feel that the stimulus has been the biggest driver to the markets where they are at. And are they overvalued? Many say yes they’re overvalued. But it is what it is, as I like to say. They can get way more overvalued before we see meaningful corrections.

So, we’re gonna stay the course. As you all know, we’ve been working very hard since before the pandemic broke out to personally manage your assets. What you’ve worked your life for. We have continued to be diligent at doing that…. spending untold 100 hundreds of hours looking at charts, looking at monetary policy, looking at liquidity models… trying to get a beat on what is happening below with the news feed. The news feed, if you listened to that, you’re going to make a lot of mistakes when it comes to investing your money.

So, we’re going to continue along those lines. If we get the additional stimulus that is on a table, if we see that the democrats control the House and Senate in the run off in January here in the United States has about $3.4 trillion of additional stimulus. So when we factor in all the stimulus again it is going to trickle to the markets. And, again we could see some fireworks going off again for much of 2021.

But in the meantime, we’re gonna stay diligent looking for any type of indicators or stresses in the system that we want to be able to avoid. We don’t have a crystal ball over here. It’s not that simple. This is a very tough game… many seasoned hedge funds and mutual fund managers have gotten their clocks cleaned this year. We’ve been relatively well. We’re going to continue to, to try to do the best we can for all of you. I encourage all of you, this weekend’s going to be pretty nice out, the sun’s shining as I’m sitting in my home office. I’m going to get outside, hopefully get a run in here later this afternoon.. encourage all of you to get outside this weekend, get some sunshine, get some fresh air, and WE’LL deal with 2020 as we go day by day. Nothing more, nothing less. If you need anything, please give me a call. I look forward to talking with you if you have any concerns at all. Be safe. Be careful. And again, enjoy the weekend. Take care. Bye bye.

Market Update 10-28-2020

Please note, this video was recorded on Tuesday, 10/27/2020.

Video Transcript:

Hello everyone! I hope this video finds you well and healthy. It’s Tuesday afternoon and I just want to get a video out to all of you in light of the election coming up and maybe address some concerns you may have about what I’m thinking or what I’ll be looking for during this period.

Well, it can be a time of volatility, but the markets have been relatively calm here lately. We’ve been in a pretty tight range from September… up and down, up and down, but staying in a relatively tight range in the indexes and we suspect that to continue for the near future.

We want to let you know we are still continuing to spend a lot of effort and time in looking at the charts, looking at the liquidity flows from a monetary standpoint in and out of the markets, the overall economy itself what it what is happening there. We see that there continues to be a large stimulus in the economy; it will continue to be there for the foreseeable future of liquidity infused into the system from the Federal Reserve. Charts are all pretty healthy, not only with companies here in America and indexes here in America, but we’re seeing around the globe pretty healthy charts and seeing some breadth increase, meaning the participation by other sectors here of late, which is a healthy, healthy thing to see happen… we think that’s going to continue. We still feel that the markets will be higher by the end of this year – a lot based on the stimulus that is in the system…. less and less places for people to find places to invest money in and get some type of return that is meaningful. Here in the US, and the US indexes, is one of those places where the globe looks for that investment. So we can think it’s going to continue to be strong through the rest of the year.

Certainly due to the presidential election, we could again see some volatility. But overall, most people don’t want to believe this, but very few presidents have a meaningful impact on the economy based on what history says. As we look back through history, back to Eisenhower, we’ve only seen two presidents with negative returns…. that being George Bush and President Ford’s tenure in office is the only four year period, and when it came to George Bush, an eight year period, where there was a negative return. And the rest have been all positive returns for the markets… and we’re talking in particular the S&P 500 in this instance. It has been some very, very strong periods to be invested in the market. President Clinton had over a 200% return on your money during his eight year tenure. President Obama, he had about a 182% return over his time in office. So again, we’re seeing that who’s in office can have some effects, more volatility than overall market returns.

So, looking long term, again, the place to be is generally in the markets based on what you can handle and what your risk tolerance is.

Could we have some volatility creep up? Yes.

If we see that Joe Biden becomes president, are there gonna be some things that we want to look at from a planning standpoint or an investment standpoint that we’d want to change? Yes.

If President Trump stays in office, will we look for opportunities or any type of changes under his tenure that we can take advantage of? Yes.

So it really doesn’t matter to us in how we’re going to manage your money, we’re going to look for opportunities. We’re going to try to find the places that we feel that we can get a reasonable return for the risk that we’re taking and continue to look to grow your assets over time and not put you through any type of major drawdown in your portfolios. We’ve done been pretty good at that – managing drawdowns here the last several years. And we will continue to be diligent at that. But, we still have to have market exposure to grow your portfolios.

So, to sum everything up: we’re not super aggressive right now in the markets. We are sitting by ready to make any changes, whether it is to reduce our exposure in the markets and raise cash, or to go in heavier into the markets. We’re ready to do either/or, but at this point we are invested in the markets. We’re going to continue to be invested in the markets through the election, unless again some things change here over the next several days, which can happen. But we’ll be ready to adjust to those changes.

So I just wanted to get this out to let you know that we’re working hard. The amount of time that we’re spending looking at your portfolio’s has not been reduced at all. Again, as I’ve said in past videos, this is a war getting through COVID. It’s a war, and lots of battles are going to be fought through this war until we get through this. And so we just got to make sure we win more battles than we lose so that we win the war. And that’s what we’re going to continue to do… be diligent and making sure that we do the very best job for all of you.

You deserve it.

You put your trust in us, handling your wealth, and we take it very serious and we’re going to continue to be really diligent and work hard. If you have any concerns, any questions about anything you’re seeing or hearing or anything to do with your portfolio, please give me a ring… give me a call. We look forward to speaking with you. And if there’s anything that we can do to help you or you need, please reach out to me or Kelsey; we’ll do our best to make sure we we help in any way possible. Take care. And we look forward to speaking with all of you soon. Bye bye.

Brent Chavez

Investment Advisor Representative

bchavez@aeinvestmentsgroup.com

Market Update 9-20-2020

Video Transcript:

Good afternoon, everyone. I hope this finds you all doing well and staying healthy. It is Saturday afternoon. It is a beautiful Saturday afternoon the sun is shining. It is a bit chilly for my liking I kind of like it hot and humid. So I’m a little bit not liking this weather at all… but I hope you are doing well.

I want to update about what is going on, what we’re seeing in the markets. What am I thinking what am I looking at moving forward. I’m sure many of you have had some concerns over the last two weeks, because of the market action. We have seen the NASDAQ, as of close Friday, down over 10% from its all time high. We’ve seen the S&P 500 pull back over 7% from its all time high. And the Dow Jones pulling back over 5%. So there’s a lot of ruckus and noise as to why this pullback is happening.

As we look around at the charts we see that there’s a lot of strength, not just in the US, we’re seeing this strength globally. We’re seeing it more as a rotation out of tech and into things like materials. We’re seeing a rotation even into what has been a dog… the financials – a lot of money flowing towards that area in the last several weeks. And as we move forward, we think that you know that rotation may stick this time. In the past that rotation has been a head fake and everybody starts piling back into those tech names and driving them higher.

At this point, my feeling is that this may be a little bit stickier and we may get a continued rally in these areas that have greatly underperformed this bull run we’ve had since March lows. But again, all of this is actually healthy for the overall markets to continue higher. We have countries that are participating like Switzerland, Denmark, Sweden, Japan, Taiwan… all time highs. So we’re seeing a breadth expanding of what is happening in the markets.

So again, all healthy in pointing that the trend higher is still in place. In fact there’s some very well respected analysts that are saying markets may be shockingly higher by the end of the year. And whether it makes sense or not, we can’t worry about that. We just want to make sure we have you on the right side of whatever the market is going to be doing. And the last several weeks we’ve not been on the right side a little bit because markets have been quite tricky to say the least. We do have models that we have been using, liquidity models. Those models were pointing at the end of August to a pullback but it didn’t happen in the timing of the models. And again, models are just that… models. They forecast much like the weather forecast. And sometimes the weather forecast is wrong.

And so, again, when it comes to the models we’re looking at, a lot of that can be attributed to the fact that the Federal Reserve has just put so much liquidity into the system. The central banks around the globe have put trillions and trillions of dollars of liquidity into the economy. So, that has no doubt skewed what should be happening in the markets. But it is what it is. So again, we just want to make sure we’re on the right side of that.

And so the models delayed by about two weeks and that kind of threw us off from getting more defensive. We had been prepared at the end of August with a lot of cash but then the markets kept running so we went in on the long side pretty heavy. Then when we started to get a pullback in mid September I really wasn’t sure that it was a real deal that we’re going to see much of a pullback. And so we really didn’t want to get involved in chasing this down and trying to time the market in such a fashion that we could exacerbate any losses we had in the portfolio.

So, at this point, we are still looking at a much higher markets by the end of the year. Short term, the next two weeks from a seasonality standpoint, are very difficult historically speaking. But again, with the liquidity that’s been put into the system, we don’t know how much of that downside is continued. But we are prepared to protect to the downside if we see continuation of where these markets sit as a close of Friday. We may potentially add to the long side if we see the markets looking like they want to do a turnaround and start going back up.

Day-by-day, hour-by-hour sometimes we are exhausting ourselves with trying to look at charts and looking at models. Looking at the data that is coming in, for the most part, it’s been pretty positive…. beating projections on where we should be with what has happened with COVID. So again, all good signs. Hopefully it can continue.

But there’s still there’s so many unknowns out there as far as what’s going to happen. There are a lot of industries that are still a disaster… travel, airlines… to name a few. Probably if the government doesn’t come in and help the airlines again, some of them are going to disappear. Last week the airlines were asking for about $25 billion to continue to get them through this crisis and they said if they don’t, there will be massive layoffs. So again, there still are many problems we’re facing.

Could we have a second coming of COVID-19 that causes problems as far as overwhelming our medical facilities? We don’t know, we’ll see. Could there be a vaccine that hits soon? Probably not that soon… probably will have to get through this winter and stay the course of what all of us are trying to do to be safe, to try to distance ourselves. That’s going to affect some industries. If the government doesn’t step in and help them and provide more liquidity to them, probably some of them may may have to go bankrupt… but we’ll see. There may be you know that may be the next wave of problems… economies, bankruptcies to companies that have really suffered during COVID. But again, things that we have to wait and see at this point.

So, just wanted to give you an update because again I’m sure many of you are wondering what’s going on. But just to recap, we are looking to get defensive here in the next couple of weeks… if we have to, to put some hedging on. We’re prepared to add to our longs if things look like they’re clearing up. But again, day-by-day.

I’d like to thank all of you for being part of our family of AE and letting us take care of something that is so important to you, your financial future. We want to thank you for that. We take it very seriously, working very hard and we’ll continue to be diligent until we get through this crisis.

If you need anything, please feel free to reach out to me, give me a call. I will do anything I can to help you. Hope you have a wonderful weekend. Get outside. It’s beautiful. You may have to wear a jacket, maybe even a hat and some gloves, but get outside, get some fresh air in and enjoy the beauty around. Take care. We’ll talk to you all soon. Bye.

Should You Care What the Financial Markets Do Each Day?

Focusing on Your Strategy During Turbulent Times.

Investors are people, and people are often impatient. No one likes to wait in line or wait longer than they have to for something, especially today when so much is just a click or two away.

This impatience also manifests itself in the financial markets. When stocks slip, for example, some investors grow uneasy. Their impulse is to sell, get out, and get back in later. If they give in to that impulse, they may effectively pay a price.

Across the 30 years ended December 31, 2018, the Standard & Poor’s 500 posted averaged annual return of 10.0%. During the same period, the average mutual fund stock investor realized a yearly return of just 4.1%. Why the difference? It could partly stem from impatience.1

It’s important to remember that past performance does not guarantee future results. The return and principal value of stock prices will fluctuate over time as market conditions change. And shares, when sold, may be worth more or less than their original cost.

Investors can worry too much. In the long run, an investor who glances at a portfolio once per quarter may end up making more progress toward his or her goals than one who anxiously pores over financial websites each day.

Too many investors make quick, emotional moves when the market dips. Logic may go out the window when this happens, in addition to perspective.

Some long-term investors keep focus. Warren Buffett does. He has famously said that an investor should, “buy into a company because you want to own it, not because you want the stock to go up.2

Buffett often tries to invest in companies whose shares may perform well in both up and down markets. He also has famously stated, “If you aren’t willing to own a stock for ten years, don’t even think about owning it for ten minutes.”2

In contrast with Buffett’s patient long-term approach, investors who care too much about day-to-day market behavior may practice market timing, which is as much hope as strategy.

To make market timing work, an investor has to be right twice. The goal is to sell high, take profits, and buy back in just as the market begins to rally off a bottom. But there is volatility in financial markets and the sale at any point could result in a gain or loss.

Even Wall Street professionals have a hard time predicting market tops and bottoms. Retail investors are notorious for buying high and selling low.

Investors who alter their strategy in response to the headlines may end up changing it again after further headlines. While they may expect to be on top of things by doing this, their returns may suffer from their emotional and impatient responses.

Nobel Laureate economist Gene Fama once commented: “Your money is like soap. The more you handle it, the less you’ll have.” Wisdom that may benefit your strategy, especially during periods of market volatililty.3

How have your investments performed through these turbulent times?

Questions? Please do not hesitate to contact us: info@aeinvestmentsgroup.com, (215) 766-7002

Citations

1 – nytimes.com/2019/07/26/your-money/stock-bond-investing.html [7/26/19]

2 – fool.com/investing/best-warren-buffett-quotes.aspx [8/30/19]

3 – suredividend.com/best-investment-quotes/ [12/5/18]

Mutual funds are sold only by prospectus. Please consider the charges, risks, expenses and investment objectives carefully before investing. A prospectus containing this and other information about the investment company can be obtained from your financial professional. Read it carefully before you invest or send money.

This material was prepared by MarketingPro, Inc., and does not necessarily represent the views of the presenting party, nor their affiliates. This information has been derived from sources believed to be accurate. Please note – investing involves risk, and past performance is no guarantee of future results. The publisher is not engaged in rendering legal, accounting or other professional services. If assistance is needed, the reader is advised to engage the services of a competent professional. This information should not be construed as investment, tax or legal advice and may not be relied on for the purpose of avoiding any Federal tax penalty. This is neither a solicitation nor recommendation to purchase or sell any investment or insurance product or service, and should not be relied upon as such. All indices are unmanaged and are not illustrative of any particular investment.

Investing for Impact

Socially responsible investment strategies and you.

SRI (Socially Responsible Investing), Impact Investing, and ESG (Environmental, Social, and Governance) Investing belong to a growing category of investment choices that use traditional investing practices to responsibly impact society.

In the past, these investment strategies were viewed as too restrictive for most investors. But over time, improved evaluative data and competitive returns have pushed these strategies into the mainstream. Even though SRI, ESG investing, and impact investing share many similarities, they differ in some fundamental ways. Read on to learn more.1

ESG Investing assesses how specific criteria of an investment, such as its environmental, social, and governance practices, may impact its performance. These factors are used in an evaluative capacity. In the United States alone, there are more than 350 ESG mutual funds and ETFs available.2,3,4

SRI (Socially Responsible Investing) uses criteria from ESG investing to actively eliminate or select investments according to ethical guidelines. SRI investors may use ESG factors to apply negative or positive screens when choosing how to build their portfolio. For example, an investor may wish to allocate a portion of their portfolio to companies that contribute to charitable causes. In the U.S., more than 12 trillion dollars are currently invested according to SRI strategies.4,5

Impact Investing or thematic investing differs from the two above. The main goal of impact investing is to secure a positive outcome regardless of profit. For example, an impact investor may use ESG criteria to find and invest in a company dedicated to the development of a cure for cancer despite whether success is guaranteed.6

The biggest take away? There have never been more choices for keeping your investments aligned with your personal beliefs. But no matter how you decide to structure your investments, don’t forget it’s always a smart move to speak with your financial professional before making a major change.

Citations

1 – https://investor.vanguard.com/investing/esg/ [01/01/2020]

2 – Investing in mutual funds is subject to risk and potential loss of principal. There is no assurance or certainty that any investment or strategy will be successful in meeting its objectives. Investors should consider the investment objectives, risks, charges, and expenses of the fund carefully before investing. The prospectus contains this and other information about the funds. Contact the fund company directly or your financial professional to obtain a prospectus, which should be read carefully before investing or sending money.

3 – Exchange Traded Funds (ETFs) are subject to market and the risks of their underlying securities. Some ETFs may involve international risks, which include differences in financial reporting standards, currency exchange rates, political risk unique to a specific country, foreign taxes and regulations, and the potential for illiquid markets. These factors may result in greater share price volatility. ETFs that focus on a small universe of securities may be subject to more market volatility as well as the specific risks that accompany the sector, region or group. An ETFs trading price may be at a premium or discount to the net asset value of the underlying securities.

4 – https://www.morningstar.com/content/dam/marketing/shared/pdfs/sustainability/Sustainable_Funds_Landscape_2018.pdf?cid=EMQ_ [02/04/2019]

5 – Asset allocation is an approach to help manage investment risk. Asset allocation does not guarantee against investment loss.

6 – https://www.ussif.org/sribasics [08/02/2019]

This material was prepared by MarketingPro, Inc., and does not necessarily represent the views of the presenting party, nor their affiliates. This information has been derived from sources believed to be accurate. Please note – investing involves risk, and past performance is no guarantee of future results. The publisher is not engaged in rendering legal, accounting or other professional services. If assistance is needed, the reader is advised to engage the services of a competent professional. This information should not be construed as investment, tax or legal advice and may not be relied on for the purpose of avoiding any Federal tax penalty. This is neither a solicitation nor recommendation to purchase or sell any investment or insurance product or service, and should not be relied upon as such. All indices are unmanaged and are not illustrative of any particular investment.

Video Transcript:

Hello everyone. Brent Chavez, Aequitas Equitas Investment Group. We’re just duking it out with the markets over here in the war room. We want to let you know that we are staying on top of what’s happening in the economy in the markets, and we’re trying to do our best to navigate through this for all of you.

We appreciate all of you as our clients and we really want to try to make the best possible decision with your portfolio’s at this time. We’re still very heavy into cash for most of you: upwards of 40% cash, 10% treasuries, and then 10% utilities. For most of you, about 60% of your portfolio is still very defensive. Some of you, because of age, are going to be different or income needs would have a different portfolio build, but overall, that’s where we stand for most of you.

So, I just want to update you. Monday was a brutal day. Last week, it looked like we were going to get some sideways action that, at least in the markets, technicals had cleaned up. As I said on a video, we had kind of dipped our toes into the water with some stocks that really had shown some real relative strength – they held up the best during that 14-day down period that we saw… so, we added a little bit of that to our portfolios.

So, we’re going to update you today. It’s Tuesday. What has happened?

We see the S&P 500 down year-to-date, in the purple, 16%, and the Dow Jones Industrial, in the blue, is down 17%. Most of our portfolios are down less than 3% year-to-date – so, what we’re doing is good. That is as good as anyone could expect in these conditions and we’re going to continue to try to manage so that we can make the best decisions moving forward.

A couple things that we’re looking at, again yesterday, we saw that ugly day down. Why? OPEC and Russia got into an oil war… ugly for the markets… ugly for a lot of portfolios… but good for the consumer overall. You know we have to look at the light at the end of the tunnel. We’re going to get much lower gas prices here moving forward. We’re going to get lower heating oil bills and a lot of things we’re consuming are going to be cheaper because of that. So let’s take the good with the bad and remember that there’s always going to be an opportunity for us moving forward, to find ways to hopefully make some money for all of you.

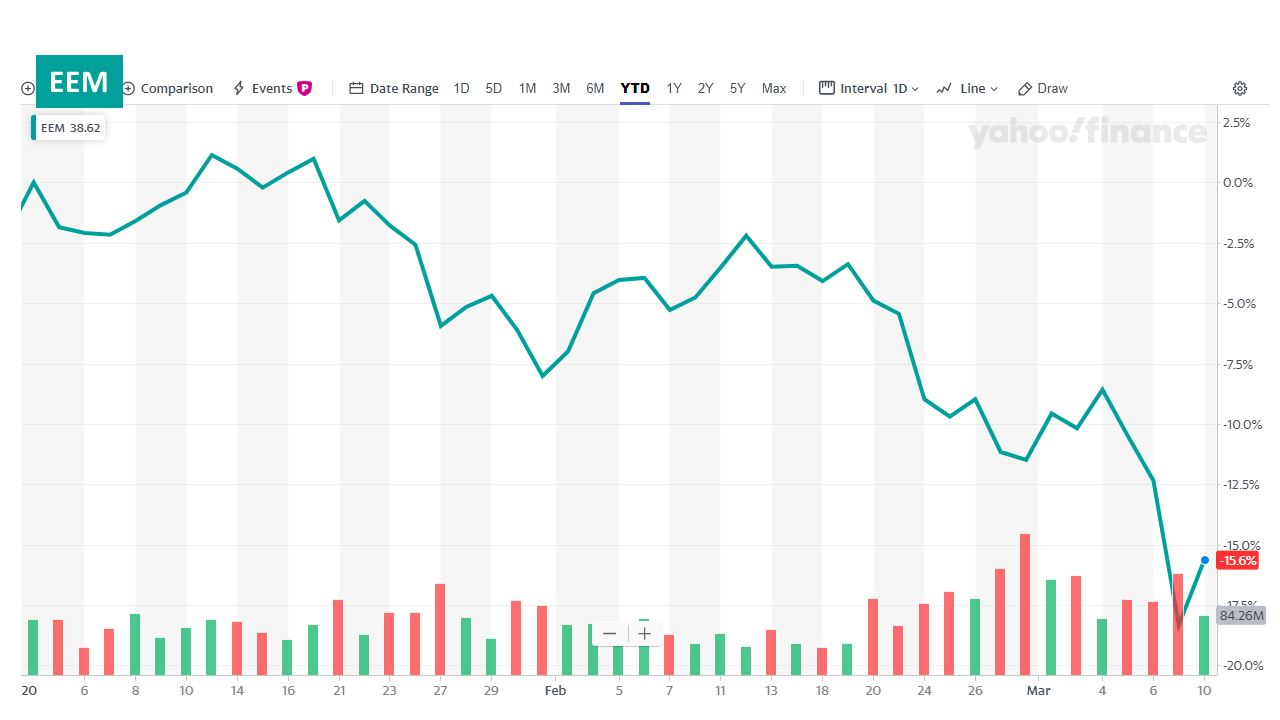

We’re going to look at some things that we’re looking at for global health. Emerging markets for one and the price of copper. We’re looking at many other things, but I just want to highlight two of the things we’re looking at in this video.

Here’s emerging markets.

Interesting story about emerging markets. Emerging markets, you would think would be down maybe 25 or 30% year-to-date. Again, these are countries that are undeveloped with very small economies, very small companies – only down 15.6% year-to-date. That is one of the things we looked at last week as to why we were dipping our toes in because the relative strength in emerging markets showed in the face of a very ugly and brutal sell off – held up very well. We’re seeing it up a percent and a half or so, responding very well today.

Overall we are seeing the markets up, which is good. And we’re seeing also bond yields go up and bond prices go down. So that’s good. We want to see that. When we’re seeing green in the stock market, we want to see bonds going the other way. We want to see those yields rising… we want to see the prices falling. That’s good action that we want to see. That’s healthy action.

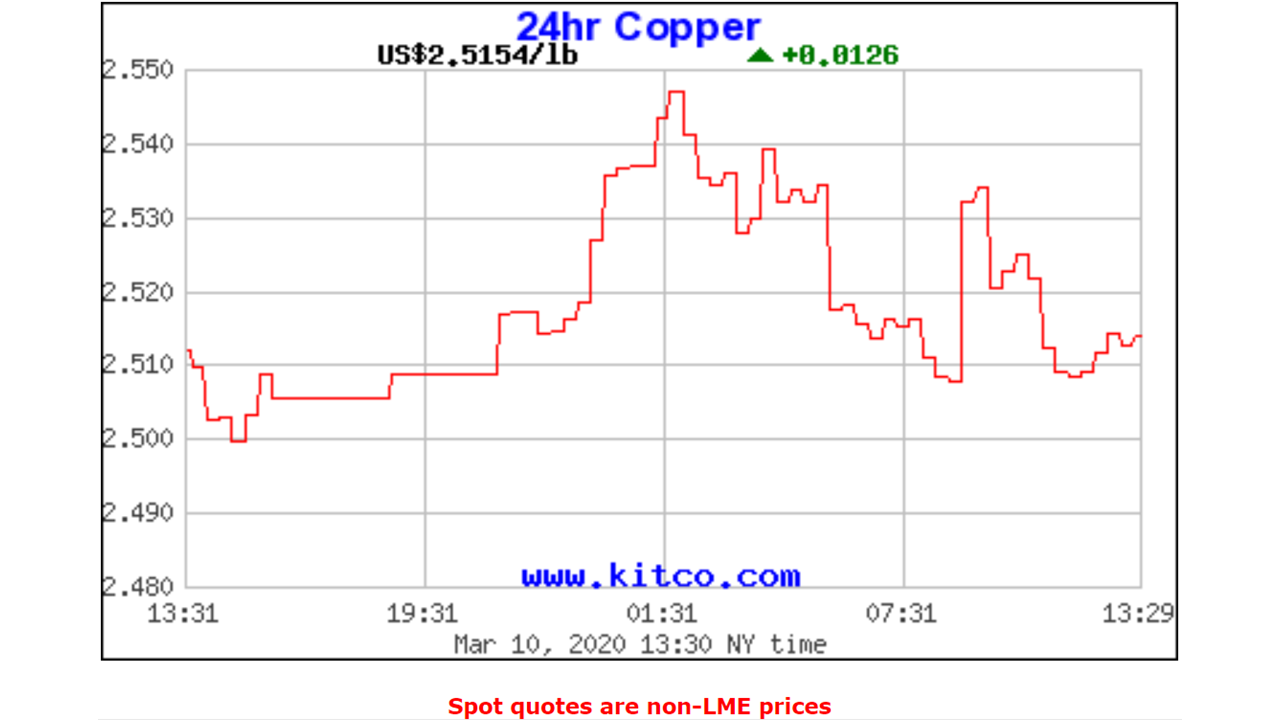

And then the other chart we’re going to share with you, the last chart, is the price of copper.

We’re looking at copper because copper will hopefully give us some type of indicator as to global activity and global consumption. And that is something that’s held up very well through this panic selling that we’ve seen around the globe. We want to see copper at about $2.55, or higher in that range to feel really comfortable that we’re not going to see another leg down and the global economy is not going to fall off the cliff. Well, as of today, we’re at about $2.51/pound. We want to see it at about $2.55 or slightly higher. We want that to be the bottom range if we want to feel comfortable that things are going to be okay.

That’s all I have for you today folks. I hope you’re doing well. As always, we’re here for you, we’re working hard. If you have any questions or concerns, feel free to reach out, give me a call and we can talk. Talk to you all soon. Take care.

Charts are from Yahoo! Finance and Kitco.com